Instructions for Completing IRS Form 1040-A (Adventurer)

Tax Year 973

Prepared by the Imperial Review Service (IRS), Kingdom of Archea

Truth, Loyalty, Documentation

WHO MUST FILE

Form 1040-A must be completed by any individual or company that acquired income through independent hazardous enterprise during the tax year.

This includes but is not limited to:

- Adventurers

- Mercenary Companies

- Licensed Tomb Robbers

- Freelance Exorcists

- Unsanctioned Heroes Seeking Retroactive Legitimacy

Taxable income includes but is not limited to income obtained through:

- Exploration

- Combat

- Salvage

- Tomb delving

- Dragon antagonization

- Heroic intervention

- Questionable heroism

- Opportunistic looting

Failure to file may result in:

- Monetary penalties

- Confiscation of undocumented treasure

- Magical audit

- Temporary detention for clarification

- Permanent documentation in the Crown’s records

GENERAL GUIDANCE

The Imperial Review Service reminds taxpayers that:

- All treasure is taxable, whether recovered from ruins, monsters, or inattentive nobility.

- Curses, ancient or otherwise, do not exempt assets from valuation.

- Treasure buried again for “safekeeping” remains taxable in the year of discovery.

Attempts to evade taxation through invisibility, extradimensional storage, planar travel, or feigned death are felonies.

RECORD KEEPING

Taxpayers are encouraged to maintain accurate documentation of deductible expenses related to adventuring activity.

Examples of such deductible expenses include:

- Equipment such as torches, ropes, pitons, bedrolls

- Healing potions

- Bribes

- Funeral costs for hirelings

- Replacement hirelings

Note that purchases of weapons, armor, and alcoholic drinks are not deductible expenses, regardless of whether such purchases were felt necessary to the continuation of the adventure at hand.

Please attach documentation for all deductions. Acceptable documentation includes:

- Merchant receipts

- Written contracts

- Witnessed statements

- Divine testimony

- Speak With Dead depositions

Statements beginning with “Trust me, bro, we totally bought a shitton of rope” are not accepted.

Failure to maintain records may result in application of the Standard Adventurer Deduction, which has historically been described by taxpayers as “punitive,” “unfair,” and “technically lawful.”

OFFICIAL REMINDER

Adventure Boldly, File Promptly

The Crown appreciates your cooperation in maintaining fiscal order within the Realm.

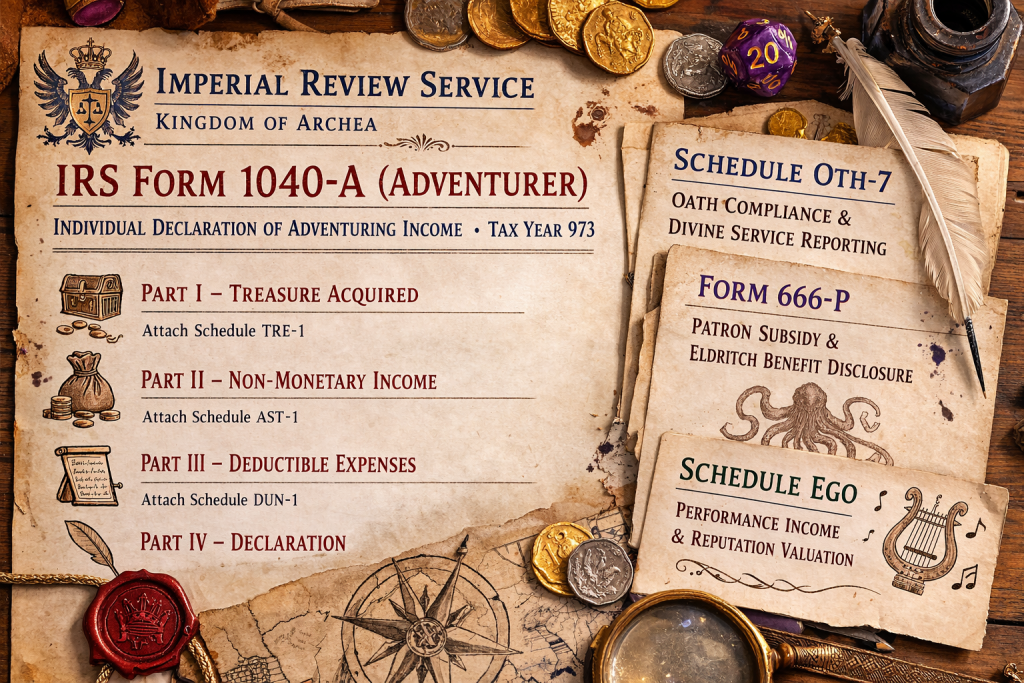

FORM 1040-A (Adventurer)

Individual Declaration of Adventuring Income

Tax Year 973

Name of Taxpayer: _______________________________

Adventuring Company Name (if applicable): _______________________________

Adventurers’ Guild Registration Number: _______________________________

Primary Profession or Class

- ☐ Fighter

- ☐ Wizard

- ☐ Paladin (attach Schedule OTH-7)

- ☐ Rogue

- ☐ Warlock (attach Form 666-P)

- ☐ Bard (attach Schedule EGO)

- ☐ Ranger

- ☐ Other: __________________

PART I — TREASURE ACQUIRED

Attach Schedule TRE-1 (Treasure Acquisition and Recovery) and report the fair market value of all treasure acquired during the tax year.

| Source of Treasure | Value (gp) |

|---|---|

| Coins and gems recovered from ruins, tombs, and inexplicably unguarded chests | |

| Coins and gems looted from bodies | |

| Property liberated from evildoers | |

| Coins and gems “recovered” after disputes with other adventurers | |

| Bounty payments received | |

| Salvage rights or dungeon claims | |

| Ancient artifacts | |

| Cursed treasure still attached to soul |

Total Adventuring Income: __________ gp

PART II — NON-MONETARY INCOME

Attach Schedule AST-1 (Non-Monetary Assets and Extraordinary Considerations).

| Asset | Estimated Value |

|---|---|

| Magic items obtained | |

| Land grants | |

| Titles or noble privileges | |

| Favors owed by powerful individuals | |

| Prophecies of future wealth |

The fair market value of all resurrections is counted as taxable income. Please attach FORM 27-R for any such events occurring in the tax year.

PART III — DEDUCTIBLE EXPENSES

Attach Schedule DUN-1 (Dungeon Delving Expenses).

- Equipment (excluding weapons, armor, and magical artifacts)

- Healing potions

- Funeral costs for hirelings

- Hazard pay for retainers

- Bribes paid to minor officials

- Therapy

- Therapy following eldritch revelations

- Therapy following bardic performances

PART IV — DECLARATION

I swear under penalty of law, divine judgment, and magical verification that this declaration is accurate and complete to the best of my knowledge.

I affirm that I have not concealed taxable assets through:

- Illusion magic

- Extradimensional storage

- Planar relocation

- Feigned death

- Clerical resurrection loopholes

I understand that knowingly submitting false information to the Imperial Review Service may result in penalties including fines, imprisonment, or extended conversation with a Senior Compliance Mage.

Signature: _______________________________

Date: _______________________________

SCHEDULE OTH-7

Oath Compliance and Divine Service Reporting

PURPOSE OF THIS SCHEDULE

Paladins derive supernatural abilities through adherence to a sacred Oath and the favor of a divine or quasi-divine authority.

The Imperial Review Service requires disclosure of oath-related activities in order to determine whether the taxpayer has received taxable benefits, divine assistance, or material support.

PART I — OATH IDENTIFICATION

Declared Oath (check one):

- ☐ Oath of Devotion

- ☐ Oath of Vengeance

- ☐ Oath of the Ancients

- ☐ Oath of the Crown

- ☐ Not entirely sure what Oath was sworn

- ☐ Other: ______________________________

Date oath was sworn (if known): __________________

Location where oath was sworn:

- ☐ Temple

- ☐ Battlefield

- ☐ Throne room

- ☐ Tavern after several drinks

- ☐ Other: __________________

PART II — DIVINE ASSISTANCE RECEIVED

Indicate any supernatural assistance received during the tax year.

- ☐ Miraculous healing

- ☐ Divine visions

- ☐ Protection from harm

- ☐ Smite-related phenomena

- ☐ Radiant explosions of unclear origin

Estimated fair market value of divine assistance: __________ gp

PART III — TITHES AND CHARITABLE ACTS

| Temple or Order | Donation (gp) | Nature of Service |

|---|---|---|

Note: Donations made after dramatic moral speeches remain deductible.

DECLARATION

I certify that the information provided above accurately reflects my oath-related activities during the tax year.

I further affirm that I have not knowingly used divine authority to obtain tax advantages, political influence, or preferential seating at taverns.

Signature: __________________________

Date: __________________________

OFFICIAL NOTICE

Paladins who violate their sworn oaths during the tax year must attach Form FALL-1 (Loss of Divine Powers Adjustment).

FORM 666-P

Patron Subsidy and Eldritch Benefit Disclosure

PURPOSE OF THIS FORM

Warlocks derive supernatural abilities through formal or informal arrangements with extraplanar entities commonly referred to as Patrons.

The Imperial Review Service requires disclosure of such arrangements to determine whether the taxpayer has received taxable benefits, gifts, or other consideration.

PART I — PATRON IDENTIFICATION

Name or commonly used designation of Patron:

________________________________________

Patron Classification (check one):

- ☐ Fiend

- ☐ Archfey

- ☐ Great Old One

- ☐ Undead Entity

- ☐ Formerly Mortal Spellcaster

- ☐ Unknown but Disturbing

- ☐ Other: ______________________________

Location of Patron (if known):

- ☐ Nine Hells

- ☐ Feywild

- ☐ Outer Void

- ☐ Inside the taxpayer’s dreams

- ☐ Unknown

PART II — BENEFITS RECEIVED

Indicate any benefits received from your Patron during the tax year:

- ☐ Eldritch knowledge

- ☐ Supernatural powers

- ☐ Visions of the future

- ☐ Whispered instructions

- ☐ Emotional manipulation

- ☐ Occasional screaming from beyond reality

Estimated fair market value of Patron assistance: __________ gp

PART III — CONTRACTUAL OBLIGATIONS

Does the Patron require any of the following from the taxpayer?

- ☐ Service

- ☐ Worship

- ☐ Occasional favors

- ☐ Unspecified future compliance

- ☐ “We will discuss this later”

If a written pact exists, attach a copy.

If the pact is written in an unknown language, please attach a translation or best effort description.

DECLARATION

I certify that the information provided above accurately reflects my relationship with the entity granting my powers.

I further affirm that I am unaware of any clauses within my pact that would result in the retroactive transfer of my soul, possessions, or descendants to the Patron without appropriate tax documentation.

Signature: __________________________

Date: __________________________

OFFICIAL NOTICE

Failure to disclose extraplanar patronage may result in penalties including fines, magical audit, or direct correspondence between the Imperial Review Service and the Patron in question

SCHEDULE EGO

Performance Income and Reputation Valuation

PURPOSE OF THIS SCHEDULE

Bards frequently receive compensation in forms that are difficult to quantify using conventional accounting practices, including applause, admiration, influence, and questionable romantic opportunities.

This schedule provides a standardized method for reporting such income.

PART I — PERFORMANCE INCOME

| Type of Performance | Location | Compensation (gp or equivalent) |

|---|---|---|

| Tavern performance | ||

| Court performance | ||

| Festival performance | ||

| Heroic ballad | ||

| Spontaneous musical number during combat |

Note: Compensation may include coin, free lodging, meals, drinks, or enthusiastic public acclaim.

PART II — REPUTATION VALUATION

- ☐ Unknown

- ☐ Locally recognized

- ☐ Regionally admired

- ☐ Widely celebrated

- ☐ The subject of multiple songs (some accurate)

Estimated value of reputation-based benefits received this year: __________ gp

PART III — BARDIC INSPIRATION DISTRIBUTION

Number of times Bardic Inspiration was provided during the tax year: __________

Did any recipients subsequently achieve financial gain, heroic status, or romantic success?

- ☐ Yes

- ☐ No

- ☐ Unclear but likely

DECLARATION

I certify that the income reported above represents a reasonable estimate of my artistic earnings and public reputation.

I further affirm that any exaggerations present in this document are no greater than those typically found in bardic storytelling.

Signature: __________________________

Date: __________________________

OFFICIAL NOTICE

Taxpayers who attempt to claim “being extremely charming” as a deductible expense will be referred for further review.

FORM 27-R

Resurrection Event Reporting

If the taxpayer died during the tax year and later returned to life, please complete this form (a separate form is required for each episode).

Cause of death (check all that apply):

- ☐ Dragon

- ☐ Trap

- ☐ Wizard experiment

- ☐ Friendly fire

- ☐ Accounting dispute

- ☐ Other: __________________

Cleric performing resurrection: __________________

Temple receiving donation: __________________

Value of resurrection service: __________________ gp